Employee - FAQ

What is a 401(k) plan?

A 401(k) is a retirement plan designed to help employees save for retirement. The rules and regulations for the 401(k) plan can be found in section 401(k) of the IRS tax code (imagine that!). Employers typically sponsor a 401(k) plan to be made available to employees as a benefit to help save for retirement.

The primary advantages of saving for retirement using a 401(k) is the opportunity to defer taxes on contributions and allow the money to grow until it is needed in retirement. Some employers also offer matching contributions, which can lead to additional growth of the money in the plan.

What is an employer match?

An employer match is when the employer makes contributions to participant accounts based on a predefined formula. As an example an employer may commit to match participant contributions dollar-for-dollar up to 3% of total compensation for the participant.

If the participant made $40,000 in income for the year and contributed 3% of their salary, then the employer would make a matching contribution of 3% to the participant’s account.

Participant Contribution: $40,000 x .03 = $1,200

Employer Match Contribution: $1,200 <----- 3% of total compensation

Total Contributions for Year: $2,400

In this example the participant was able to have an additional $1,200 contributed to their retirement account on top of their contribution (awesome!).

Employer matching contributions can be a great way for employees to receive additional contributions towards their retirement savings while utilizing the 401(k) plan benefits.

Each plan may have its own rules and guidelines regarding employer matching contributions. It is recommended to reach out to the plan administrator to get a full understanding of the requirements and potential vesting limits.

What is vesting and how does it impact me?

Vesting refers to the percentage of ownership a retirement plan participant has in relation to employer matching contributions made to their account. The vesting requirements and percentages are outlined in a vesting schedule and are typically based on the years of service a participant has accumulated while working for the employer offering the retirement plan.

For example, a vesting schedule may require employees to complete two years of service to become 100% vested for employer contributions made to their account.

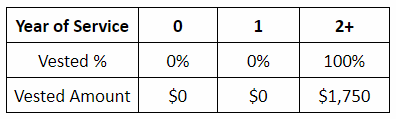

If a participant received an employer matching contribution in year 1 for $1,750, their vesting schedule would be

If the participant were to leave the employer after one year of service, they would not be able to take any of the employer matching contributions made to their account. After completing two years of service the participant will be 100% vested for both current and future employer matching contributions.

How much can I contribute to a 401(k)?

Each year the Internal Revenue Service (IRS) sets the maximum amount of money that can be contributed to a 401(k) plan. For tax year 2025 401(k) plan participants can contribute the following based on age:

Age 49 and under: $23,500

Age 50 and over: $23,500 + $7,500 = $31,000

Participants 50 year of age and older can make “catch-up” contributions to a 401(k) plan which allows for an additional $7,500 in contributions on top of the existing limit of $23,500 for tax year 2022.

What can I do with funds in an old employer 401(k)?

There are a variety of options available for funds in your old 401(k) which include:

- Leaving your money in the old 401(k) plan

- Rollover the money into your current employer’s 401(k) plan

- Rollover the money into an Individual Retirement Account (IRA)

- Cash out the money (taxes and penalties may apply)

Talk to your current 401(k) plan provider if you are interested in rolling money from an old 401(k) plan into your current 401(k) plan.

What is the difference between pre-tax and Roth contributions made to a 401(k)?

Depending on the retirement plan design, participants may be able to make either pre-tax or Roth contributions to their account.

A pre-tax contribution allows participants to defer paying taxes on the money they contribute to the 401(k). By deferring taxes, the money has the potential to grow at a greater rate and also reduce the amount of income taxes paid in the current year. When the participant retires they pay taxes on the money and earnings that are withdrawn from the 401(k) account.

A Roth contribution is made with money that has already been taxed. The money is then able to be invested in the same manner as pre-tax contributions. The major difference with Roth contributions is that when the participant withdraws the funds in retirement they may avoid paying income tax on the distributions if they have maintained the account for 5 years and are age 59 1/2 or older. Additionally, Roth contributions do not reduce the income tax amount due for a participant in the year the contribution is made, which is what occurs for pre-tax contributions.

Why should I start saving if I won’t retire for many years?

Starting to save as early as possible for retirement provides the opportunity for money to grow over a long period over time, which can greatly increase the chances for a comfortable retirement. The power of compounding allows for even the smallest amounts of money to grow exponentially over time when invested on a regular basis.

For example:

Employee A and Employee B work at the same employer and are the same age. Employee A starts savings $150 per month for retirement at age 25, while Employee B starts saving $250 for retirement at age 35. Both plan to retire at age 65.

Assuming a 5% rate of return on investments, the ending retirement balance for each participant at age 65 is:

Employee A – $228,903.02 <--------- $150 per month starting at age 25

Employee B – $208.064.66 <--------- $250 per month starting at age 35

Difference = $20,838.36

By starting to save for retirement earlier, Employee A was able to save more for retirement while contributing a smaller amount from their monthly paycheck.

What is a rollover?

A rollover is a transfer of funds from one retirement account to another. Rollovers can be performed in a combination of ways including:

- Previous employer 401(k) plan to current employer 401(k) plan

- Previous employer 401(k) plan to IRA

- IRA to IRA

- IRA to current employer 401(k) plan

Certain rules and restrictions may apply when performing the various types of rollovers so be sure to understand the implications. Contact your current 401(k) plan provider for additional information about your rollover options.

What is auto-enrollment, and how does it impact participants?

Employer sponsored retirement plans may offer auto-enrollment which means employees that become eligible for the retirement plan are automatically enrolled and a certain percentage of their wages are contributed to the plan. Eligibility to be able to contribute to a 401(k) is usually defined as a time period an employee must wait (i.e. 90 days). Once the employee completes the specified time period they are then eligible for contribute to the 401(k). Employees can elect not to contribute or to adjust the percentage of pay to a different amount.

Can I still save for retirement if my employer doesn’t offer a 401(k)?

Yes! The most common way to save for retirement for employees without an employer sponsored retirement plan are through the use of an Individual Retirement Account (IRA). An IRA allows people with earned income to set aside money in an account similar to a 401(k) that has the potential to offer tax deferred growth over time.

I am nearing retirement, what actions can I take to help me prepare?

Nearing retirement can be an exciting time, but it’s also a time when having grasp of your current and future financial needs are of the utmost importance. Some actions you can take to get ready for retirement are:

- Make a Plan – Create a budget for both short-term and potential long-term needs in retirement. Factor in any large expenditures you may have in retirement (i.e. vacation, donation, health care).

- Take Inventory – Identify all of the assets you currently have and whether or not they will sustain your lifestyle in retirement. Also, examine your current insurance coverage and ensure it provides the appropriate amount of coverage.

- Know Your Options – Examine various retirement scenarios, such as working longer or delay claiming Social Security, and determine which option works best for you.

Planning for a successful transition into retirement can feel like a daunting task but taking the time to understand your options can greatly increase your chances for success.

Distributions from traditional IRAs and employer sponsored retirement plans are taxed as ordinary income and, if taken prior to reaching age 59½, may be subject to an additional 10% IRS tax penalty.